Even if things seem too good to be true on Wall Street, history shows that they probably are.

For most of the past 16 years, the U.S. stock market has been on a roll. Other than the five-week coronavirus crash and the nearly nine-month 2022 bear market, investors have been immersed in a secular bull market.

This year, we’ve seen the broad-based S&P 500, the growth-driving Nasdaq Composite, and the iconic Dow Jones Industrial Average all rise to multiple all-time highs. These gains have been driven by advances in artificial intelligence, expectations for future interest rate cuts by the Federal Reserve (lower interest rates lower borrowing costs for companies and can act as a catalyst for hiring, innovation, and merger and acquisition activity), and better-than-expected corporate profits.

The stock market may have its limits, but history offers two different perspectives. Over the past century, stocks have delivered some of the highest average annual returns of any asset class, but these gains haven’t come without hiccups along the way.

As the S&P 500, Nasdaq Composite and Dow Jones Industrial Average rise to unprecedented levels, stock valuations are set to follow suit.

Wall Street appears to be heading into the new year with the second-highest stock market in history, but history is giving investors dire warnings about what’s to come.

The stock market has only gone up once since 1871

Before we proceed, let’s add an important modifier. There are no data points, indicators, or correlated events that can guarantee what an individual stock or stock index will do in the short term. If something like this existed, all investors would use it to predict the future.

Nevertheless, history has a way of rhyming on Wall Street. Some correlated events in history have a good track record of predicting the future of the S&P 500, Nasdaq, and Dow Jones.

Ratings are usually completely subjective. What you think is overpriced may be seen as a bargain by another investor. Every investor has their own process of valuing stocks, which leads to an unpredictable market.

But there is one metric that leaves little room for debate. That is the Shiller price-to-earnings (P/E) ratio for the S&P 500, also known as the cyclically adjusted P/E ratio (CAPE ratio).

What makes the Shiller P/E ratio so valuable from a valuation perspective is that it is based on average inflation-adjusted returns over the past 10 years. While the traditional P/E ratio, which is based on earnings per share over the past 12 months, can easily change due to shock events or economic downturns, the Shiller P/E ratio remains useful during these events.

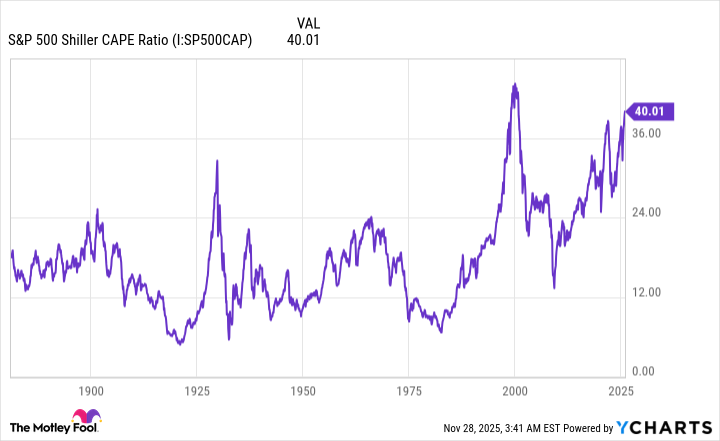

S&P 500 Shiller CAPE Ratio data by YCharts.

Although the Shiller PER was not formally introduced until the late 1980s, it has been backtested as far back as January 1871. The average multiple for the past 155 years is 17.31x.

However, as you may have noticed from the chart above, the S&P 500’s Shiller P/E ratio has been higher for most of the past 30 years than its average over the last 155 years or so. This has to do with the mainstream adoption of the Internet, which broke down the information barrier that existed between Wall Street and Main Street in the mid-1990s. Additionally, interest rates fell to historic lows in the 2010s and early 2020s, prompting investors to put money into growth stocks.

As of November 26th close, the S&P 500’s Shiller P/E was 40.20x, a stone’s throw from the current bull market’s late October peak of 41.20x. This is the third time since 1871 that a Shiller P/E high of 40 has been observed, peaking at 44.19 in December 1999 and rising several hundredths above 40 just before the 2022 bear market took shape, but only the sixth time in nearly 155 years that it has exceeded 30 during a sustained bull market. This is where historical precedent becomes important.

The S&P 500, Nasdaq Composite, and Dow Jones Industrial Average all fell between 20% and 89%, following the previous five instances in which the Shiller P/E exceeded 30. The 89% drop in the Dow during the height of the Great Depression is somewhat of an anomaly, but after the dot-com bubble burst, the S&P 500 and Nasdaq fell 49% and 78%, respectively.

Based solely on what history tells us, whether Wall Street’s major stock indexes will survive an elevator down is a matter of “when,” not “if.”

Wall Street’s moment of panic could create a generational buying opportunity for patient investors

Most investors aren’t sold on the idea that the S&P 500, Nasdaq, or Dow Jones will lose more than 20% of their value. Emotions often take the lead when red arrows rule the roost, so it’s not uncommon for these downward movements to occur quickly (i.e., elevator-down declines).

But bear markets and stock market crashes have the potential to create generational buying opportunities for investors with a long-term mindset.

As I pointed out earlier, getting from point A to point B on Wall Street doesn’t happen in a straight line. Stock market corrections, bear markets, and even worrisome crash events are normal, healthy, and inevitable aspects of the investment cycle. No matter what the Federal Reserve or the U.S. government does, nothing can prevent the stock market from occasionally experiencing this.

However, there is a notable difference in the average duration of economic downturns on Wall Street and in bull markets.

As the S&P 500 officially enters a new bull market in June 2023, Bespoke Investment Group researchers have published a dataset on X (formerly Twitter) that compares the length of all S&P 500 bull and bear markets from the beginning of the Great Depression (September 1929) through June 2023.

At one end of the spectrum, the average S&P 500 bear market resolved in 286 calendar days (equivalent to about 9.5 months). Furthermore, none of the 27 bear markets documented during this period lasted more than 630 calendar days.

By comparison, a typical S&P 500 bull market lasts 1,011 calendar days, or about 3.5 times longer than the average bear market. Additionally, about half of all S&P 500 bull markets have lasted longer than the longest bear market since the Great Depression.

While there is no way to know in advance when a stock market downturn will begin, how long it will last, or where the bottom will be, history has proven the clear benefits of jumping in during a significant stock market decline and trusting the passage of time as your ally.

Sean Williams has no position in any stocks mentioned. The Motley Fool has no position in any stocks mentioned. The Motley Fool has a disclosure policy.

The Motley Fool is a USA TODAY content partner providing financial news, analysis and commentary designed to help people take control of their financial lives. Its content is produced independently of USA TODAY.

{kind=link}