FICO includes loans that include purchase amounts in your credit report

Buy-by-buy payer loans find a location for your FICO credit score, reflecting their growing role in consumer finance. (Scripps News)

Scripps News

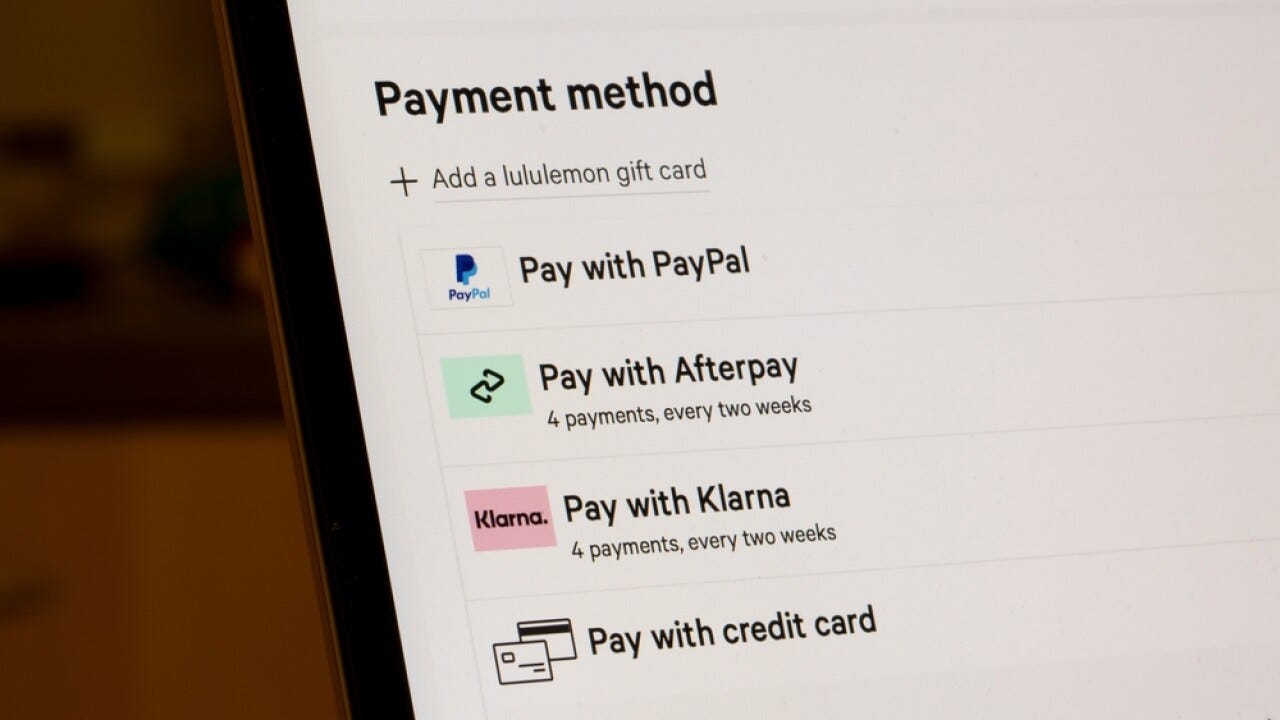

Clicking on the “Pay Later” option at checkout may affect your credit score in the coming weeks.

In February, credit scoring agency FICO announced that it would begin paying later, as well as those offered by assertions and afterpay in fall 2025, as well as those charged on credit scores with a later pay (BNPL) loan. A scoring formula that incorporates BNPL payments.

FICO scores are used in most US lending decisions and are developed based on a consistent payment history.

As FICO approaches the time to deploy a new scoring algorithm, there are things to know before your credit scores are affected.

Are you buying now or paying for a later loan?

Buy now and pay a later loan (BNPL) and offer consumers the option to pay installment purchases. Interest usually does not have minimal or minimal interest, hard credit checks, and no approval for myopia.

Services like Affirm, Klarna, Afterpay, and PayPal Pay usually offer the option to pay in the number of installments set at the online shopping checkout for consumers. Depending on the purchase and app size, consumers can choose how many payments they pay, how often they will incur, and the fees they are willing to pay. The model also offers a unique opportunity for consumers to open the same or different providers at once to open multiple loans.

Will buying now and paying a later loan affect your credit?

Until recently, one of the benefits of BNPL loans was its lack of impact on your credit score. Approval of these loans does not require a rigorous credit check. This means that consumers will not receive credit score dings to apply or use them, and were not previously reported to credit institutions as part of the official form to determine credit ratings.

Then in February, FICO announced that it would start considering BNPL loans in people’s credit scores starting in fall 2025.

FICO (Fair Isaac Corporation) is a credit scoring model with a unique algorithm that takes into account the various information contained in consumer credit department reports. It is frequently used by many major US lenders (up to 90% according to FICO).

When will you buy it and will you start to affect your credit score by paying a later loan?

FICO does not give you a specific date or timeline about when consumers begin to affect their credit scores based on BNPL data.

In a statement on September 12, FICO told USA Today in a statement on September 12 that the two credit score systems developed to incorporate the BNPL loan – a FICO score of 10 BNPL and a FICO score of 10 T BNPL- are not live yet, but “as expected, we expect it will be available this fall.”

According to FICO and previous USA Today reports, the change will not be immediately apparent to consumers.

According to FICO, lenders attempting to perform credit checks will not have access to these new score types until the relevant credit reporting agency (CRA) receives sufficient data from the BNPL provider. Lenders will not be able to use the new scoring model until the required information has been collected.

Also, consumers are unlikely to have a significant immediate impact, Nald Wallet spokesman Sarah Lasner previously told USA Today that lenders adopting new scoring would take time.

“A variety of scoring models are designed for different focus,” Lassner said. “It can take years before these are adopted primarily in decision-making and may not be adopted by lenders for any type of borrowing.”

Will buying now and paying a later loan affect my credit in the future?

As of mid-September 2025, FICO is the only credit scoring model that includes a protocol for incorporating BNPL loans into their scores.

Consumer impact depends on how the major credit institutions (Transunion, Equifax, Experian, and Private Lenders) choose to incorporate a FICO score of 10 BNPL and a FICO score of 10 T BNPL.

According to a collaborative study simulating the inclusion of BNPL data in AFFIRM, FICO found that the impact of scores was generally consistent with the opening of new accounts. It also found that the majority of consumers who declared five or more BNPL loans saw either a higher score or an impact.

“The impact of BNPL loans differs from consumer to consumer, depending on the overall credit profile of the consumer and the information contained in the BNPL loan in question,” FICO said in a statement.

FICO has also maintained this change since its first announcement that it will help “traditional, uncredit” consumers receive and improve their scores.

Lasner previously told USA Today that this could be net positive for those who are using BNPL loans responsibly.

However, the impact could soon be negative as BNPL is increasingly used for essentials rather than luxury items, and is already financially tied down. For example, a September survey by LegalShield found that 47% of BNPL customers use loans to pay for their grocery, while 35% pay for medical expenses. Almost half (49%) of BNPL users missed at least one payment, according to the survey.

“Buy now and pay later can be an incredible tool,” Lassner said.

Contributions: Rachel Barber, Medrally, USA Today

{kind=link}