We are also responsible for changes in demographics. The “Asset Reserve Depletion Date” is currently in the fourth quarter.

For most aged Americans, social security income is not a luxury. This is a necessary payment that guarantees a stable financial foundation.

For 24 years, Gallup has looked into retirees to assess their dependence on income they receive from Social Security. Each year, 80% to 90% of respondents point out that payments are a “major” or “minor” source of income. In other words, certain capabilities require you to cover the costs.

Ideally, elected lawmakers, including President Donald Trump, should do everything in their power to ensure long-term financial stability in Social Security. But based on the latest Social Security Council update, it hasn’t happened.

Worse, new analysis shows that President Trump’s flagship tax and spending law, “big, beautiful bill,” is expected to speed up cutting broad social security benefits.

Reductions in Social Security benefits could only be eight years away

Before we can dig into Donald Trump’s newly passed legislation, we need to lay the foundations for the challenges awaiting America’s major retirement programs.

Every year, since the first retired workers’ benefits were mailed in 1940, the Social Security Committee publishes a report detailing the program’s financial health in a complex way. This allows everyone to see how every income they earn is collected and track where those dollars end.

Perhaps the most important aspect of these annual reports is long-term forecasts. The long-term outlook will determine what financially sound social security will look like in the 75 years after the release of the report, taking into account changes in fiscal and monetary policy as well as ongoing demographic changes.

Since 1985, all Social Security Commission Trustee reports have warned of long-term obligations. Essentially, the projected revenue for the 75 years after the publication of the report is primarily made up of profits, but is considered insufficient to cover expenses that also include administrative expenses for running the Social Security program. As of the 2025 report, this unsubscribed obligation had risen to $25.1 trillion.

When does Social Security dry out?

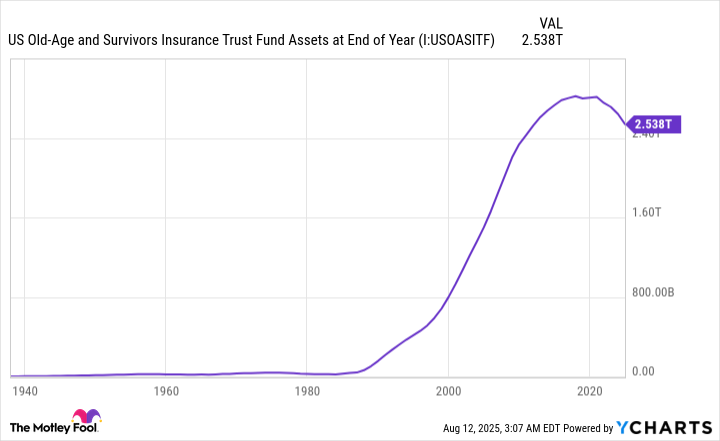

This is a difficult person, but not the most pressing cause of concern. Rather, it is the council’s prediction that the Old Age and Survivors Insurance (OASI) Trust Fund will run out of assets reserves by 2033. The OASI is responsible for monthly payments to retired workers and survivors of deceased workers.

To make it clear, it’s not One dime of assets is required to continue paying for eligible beneficiaries. However, the depletion of its asset reserves indicates that existing payment schedules, including the nearly yearly cost-of-living adjustment (COLA), are unsustainable.

The trustee’s report shows that if OASI’s asset reserves are dry, a drastic benefit reduction of up to 23% over eight years may be required.

OASI’s asset reserves are projected to be exhausted by 2033. US Old Age and Survivor Insurance Trust Fund assets are year-end data by YCHARTS.

Trump’s “big, beautiful bill” will generate profit cuts faster

However, the timeline for this projected profit reduction is not set to stone. In late July, Sen. Ron Wyden (D-OR), the Senate Finance Committee’s highest-ranking Democrat, sent a request to the Office of Social Security Chief Actuary (OACT) to decide what Donald Trump’s “Big Beautiful Building” would give to the Social Security Trust Fund.

On August 5th, OACT provided the response, updating its forecast to Senator Wyden. The headline from the OACT analysis is that Trump’s flagship law speeds up the timeline to full benefits reductions.

Specifically, the OACT analysis points to changes in tax collections that are expected to have a negative impact on Social Security programs starting this year. These changes include:

These provisions in the “large and beautiful bill” make sense, as 91% of Social Security income is collected from earned income (not wages and salaries, not wages and salaries), and an additional 3.9% comes from taxation on Social Security benefits. These aforementioned tax cut initiatives are projected to increase the costs of OASI and Disability Insurance (DI) Trust Funds by $168.6 billion from 2025 to 2034.

The expected decline in revenue is price. OASI’s new asset reserve depletion date moved from the third quarter of 2033 to the fourth quarter of 2032 on a per OACT. Hypothetically combined OASI and DI (OASDI) can potentially rely on asset reserves from DI.

Demography is also about blaming the economic struggles of social security.

While the OACT analysis finds that Trump’s “big and beautiful bill” will exacerbate the financial outlook for Social Security, it is important to recognize that the president’s newly signed law is not central to the aforementioned $25.1 trillion (and increased) long-term funding shortage. The deteriorating financial outlook for social security is primarily based on an assortment of ongoing demographic changes.

Some of these demographic changes are well known and have continued for some time. For example, baby boomers retiring from the workforce are squeezing the ratio of workers to profits.

We also witnessed a significant increase in average life expectancy since the first retired workers’ benefits checks were mailed in January 1940. The Social Security program was not designed to pay retirees for decades.

However, many of these major demographic changes occur beneath the surface.

Although it is not a demographic change, the lack of progress in the social security revision of elected lawmakers also deserves some responsibility. While there are ample proposals to strengthen social security in Capitol Hill, finding similarities between the two major American political parties has proven virtually impossible.

Donald Trump’s Tax and Expense Act is projected to make things worse for Social Security over the next decade, but it’s far from the underlying issues that need to be addressed to strengthen America’s major retirement programs.

Motley Fools have a disclosure policy.

The Motley Fool is a partner at USA Today, providing financial news, analysis and commentary designed to help people control their financial lives. The content is produced independently of USA Today.

Most retirees with the $23,760 Social Security Bonus are completely overlooked

A miscellaneous fool’s offer: If you’re like most Americans, you’re a few years (or even more) behind your retirement savings. But it’s not well known “The Secret of Social Security”It will help you to ensure a boost in your retirement income.

One easy trick can pay you an additional $23,760…Every year! Once we learn how to maximize Social Security benefits, we can retire with confidence in the peace of mind we want. participateStock AdvisorFor more information about these strategies, see

See “Social Security Secrets”»

{kind=link}