With strategic planning, you can lower your medical expenses.

Insurers cut back on Medicare Advantage

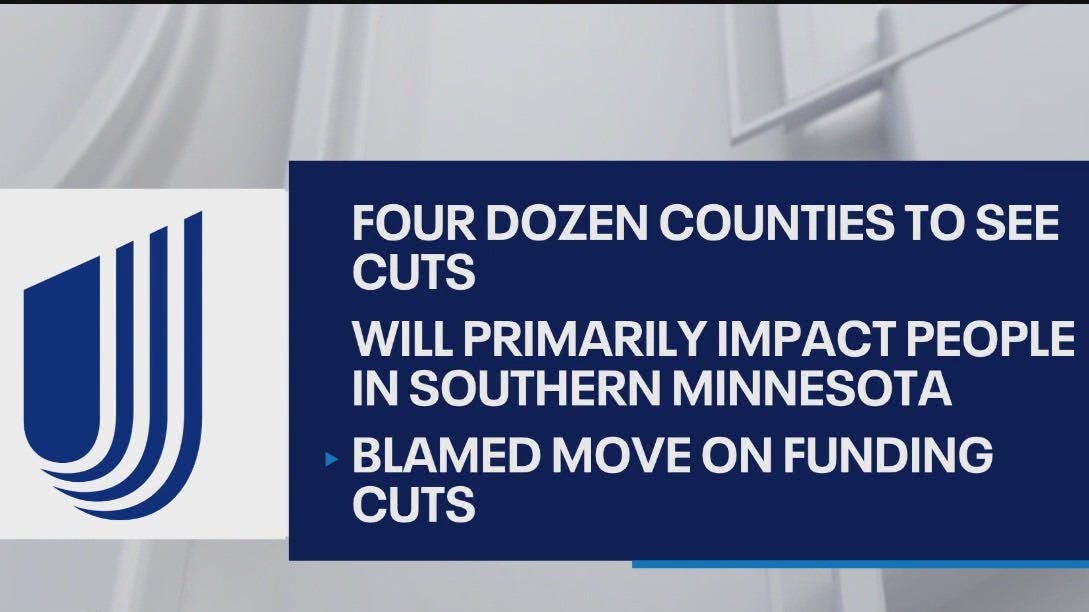

Funding cuts to Medicare will affect Minnesota residents, with UnitedHealth exiting primarily in the southern part of the state. FOX 9’s Mike Manzoni has the latest details.

Fox – Fox 9

When you retire, you may find that money is much tighter than you expected. This may be the same whether you start your retirement with a large amount of savings or a modest nest egg.

One of the biggest expenses you may face as a retiree is medical costs. Aging can be costly from a health perspective. And if you enroll in Medicare, you may find that a large portion of your monthly Social Security check goes toward medical expenses.

That’s why it’s so important to do everything you can to save money as a Medicare enrollee. Here are some strategies that can help you cut costs and ease your financial burden.

1. Avoid late registration penalties

Your initial Medicare enrollment period begins three months before the month you turn 65 and ends three months after that month. That means you have 7 months to sign up.

If you don’t enroll in a timely manner, you not only risk holes in your coverage. You also risk incurring a hefty 10% Part B surcharge every 12 months if you could have enrolled in Medicare but didn’t.

If you are still working during the initial Medicare enrollment period and have eligible group health insurance through your job, it will take longer to enroll. When you leave your job or your health insurance ends, you have a special Medicare enrollment period to take advantage of.

But otherwise, sign up for Medicare in time to avoid higher monthly premiums.

2. Review plan selections each year during recruitment.

Medicare has an open enrollment period that begins on October 15th and ends on December 7th of each year. During this period, existing Medicare enrollees can change their coverage.

Even if you’re happy with your current plan and it hasn’t changed for the worse, it’s still beneficial to review your plan options during open enrollment each year. We don’t know if there’s a better plan out there that offers better coverage and lower costs.

If your Medicare Advantage or Part D drug plan changes from year to year, that alone is reason enough to consider other plan options.

Medicare’s Plan Finder makes it easy to navigate the options available to you. Just enter where you live and the medications you take, and the tool will give you several options to choose from, along with a plan rating.

3. Take advantage of free services provided by Medicare

There are certain services available for free to all Medicare enrollees. These include annual well visits, certain vaccines, and some screening tests.

It’s important to read your Medicare coverage carefully to understand which free services you’re eligible for. By proactively addressing health problems, you may be able to avoid the high costs associated with dealing with complications that arise from poor health.

4. Stick to your Medicare Advantage plan network.

One disadvantage of Medicare Advantage over Original Medicare is that plan participants are typically limited to a specific provider network. If you go outside of your plan’s network, you may get less coverage of the services you need, or in some cases, no coverage at all.

Even worse, if you’re seeking out-of-network coverage, the amount you spend may not count toward your plan’s annual maximum out-of-pocket limit. So before you make a reservation, check your coverage, even if it’s a provider you’ve used before and your plan hasn’t changed.

However, keep in mind that Medicare Advantage plans typically require you to pay for emergency care, regardless of whether the hospital or doctor is in your plan’s network.

Medical expenses can be a major expense for retirees. Additionally, even if you are generally in good health, your medical expenses may be higher than you expected. That’s why it’s important to do everything you can to reduce your Medicare costs. And a big part of it comes down to knowing when to sign up, how to switch plans, and what rules to follow.

The Motley Fool has a disclosure policy.

The Motley Fool is a USA TODAY content partner providing financial news, analysis and commentary designed to help people take control of their financial lives. Its content is produced independently of USA TODAY.

{kind=link}